The COVID-19 has significantly disrupted key industries among Southeast Asian countries, particularly those heavily reliant on tourism and hospitality.

The virus resulted in a series of border closures, national lockdowns, and a steep rise in unemployment level, forcing the governments to release massive stimulus and accommodating spendings for the wellbeing of their countries.

2021 greets Southeast Asian countries with uncertain prospects regarding the period of economic reopenings.

While some stand upon an optimistic outlook, the achievement of optimistic forecasts mostly depends on the COVID-19 vaccine rollout implementation, management of sporadic rise in the COVID-19 cases, and exit strategy from the national lockdowns.

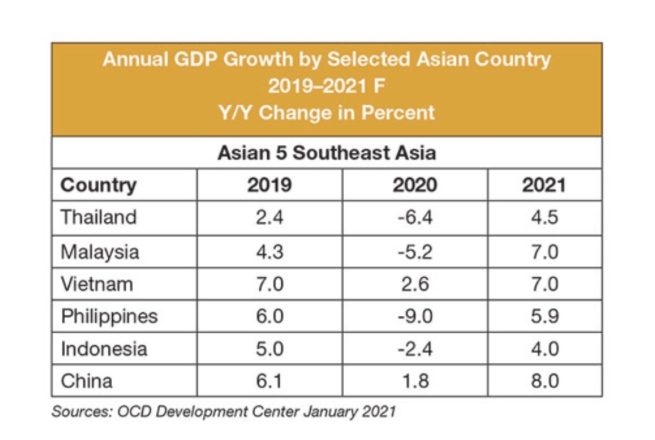

Preliminary estimates of the 2020 GDP growth of the five key Southeast Asian countries seem challenging, with only Vietnam recording a positive GDP growth compared to the previous year of 2.6%. Indonesia has recorded a retraction of -2.4% after a continuous record of approximately 5% since 2014.

Malaysia experienced a steep recession of -5.2% GDP growth, following weak performances in the previous years. Similarly, Thailand experienced a GDP fall of -6.4%. But the lowest GDP retraction was recorded in the Philippines with -9% last year.

Regardless of the recessions and weak performances in 2020 resulting from COVID-19, the five Southeast Asian countries grasped a surge of traffic for the nonwovens industry.

The massive demands for medical PPE, such as medical suits and masks, both for domestic uses and exports, have become the backbone of nonwoven substrate production.

Markets for hygiene consumer goods, such as disinfectants and cleaning wipes, have soared due to consumer behavior shifts.

The favorable demographics of emerging countries in Southeast Asia, alongside the rapidly active economic conditions, business-friendly environments, and attractive export market demands, play an essential role in positioning the region as one of the highlighted regions this year.

Economic slowdowns and short-term downside impacts in the region's manufacturing investments and consumer spending expects to rebound through accommodating stimulus programs, notwithstanding the possibility of recurring stages of the COVID-19 pandemic.

From 2015 to 2020, the development of fine denier spun bounded and spun melt polypropylene nameplate capacity in the region grew an average of 6.6% per year, with 185.000 tons in 2015 to 255.000 tons last year.

In 2020 alone, Thailand has installed 15.000 additional tons. Thailand and Indonesia have also contributed to the production of 20.000 tons each through Asahi and Toray. Moreover, Malaysia, through Fibertex, has also installed an additional 15.000 tons.

Fibertex plans to commission a Reifenhauser 5 line with an annual capacity of 15.000 tons, bringing the forecast of fine denier spunlace capacity to increase by 63.000 tons of 24.7% this year.

Southeast Asian spun bounded and spun melt refined denier producers will rely on exports to leverage the newly-established capacity utilization, considering the non-saturated emerging domestic market. Fibertex currently obtains the most considerable equity value in Southeast Asia, with a capacity of 85.000 tons.

As Southeast Asian countries enhance their production capacity, fine denier businesses seek to provide materials for nonwoven demands worldwide, relying on the shifting consumer demands to maintain the consumption of consumer hygiene products regardless of the presence of the COVID-19 pandemic.

The Latest Trends and Developments in SEA’s Digital Payments Landscape

The adoption of digital payments in Southeast Asia (SEA) has accelerated, driven by technological advancements, government initiatives, and changing consumer behaviors. It has evolved from simple online transactions to sophisticated financial ecosystems that include various payment methods such as mobile wallets, QR code payments, and Buy Now Pay Later (BNPL) options.

Digital Lending in Southeast Asia: Current Trends and Future Outlook

Digital lending in Southeast Asia (SEA) has been on an upward trajectory, significantly enhancing financial access for both individuals and businesses. The region's high internet and mobile penetration rates have facilitated this growth, enabling more people to access financial services conveniently. Governments across SEA are actively promoting digital lending as a means to improve financial inclusion, particularly for the underbanked and unbanked populations. For instance, digital lenders in countries like Indonesia and the Philippines have capitalized on the surge in internet usage to offer innovative lending solutions.

Navigating the Digital Era: Future Jobs and Skills in the Age of Digitalization

The job market's transformation driven by digitalization highlights the need to understand emerging trends and acquire essential skills for thriving.

Navigating Key Challenges in Southeast Asia’s EV Market

Southeast Asia (SEA) finds itself at a crucial juncture in the journey towards electric vehicle (EV) production and adoption as the world transitions towards sustainable transportation solutions. The region has several significant keys for developing the EV industry, such as Indonesia's nickel supply and Thailand's EV manufacturing potential. However, the ASEAN EV industry faces many challenges and threats that must be overcome to ensure success in the region.